Codirectors

Ralph S. J. Koijen is the AQR Capital Management Professor of Finance at the University of Chicago Booth School of Business. His research focuses on finance, insurance, and macroeconomics. He has been an NBER affiliate since 2010.

Sydney C. Ludvigson is the Julius Silver, Roslyn S. Silver, and Enid Silver Winslow Professor of Economics at New York University. Her research focuses on the interplay between asset markets and macroeconomic activity. She has been an NBER affiliate since 2003.

Featured Program Content

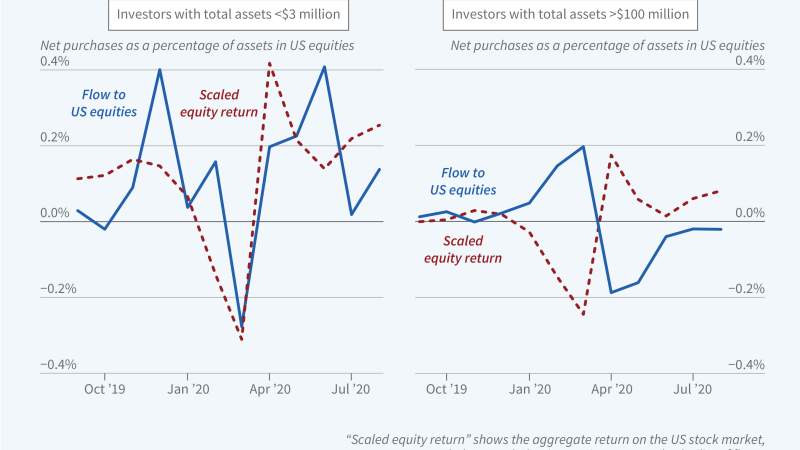

How investors adjust their portfolios in response to movements in asset prices and other shocks is a key input to asset pricing models, yet data limitations...

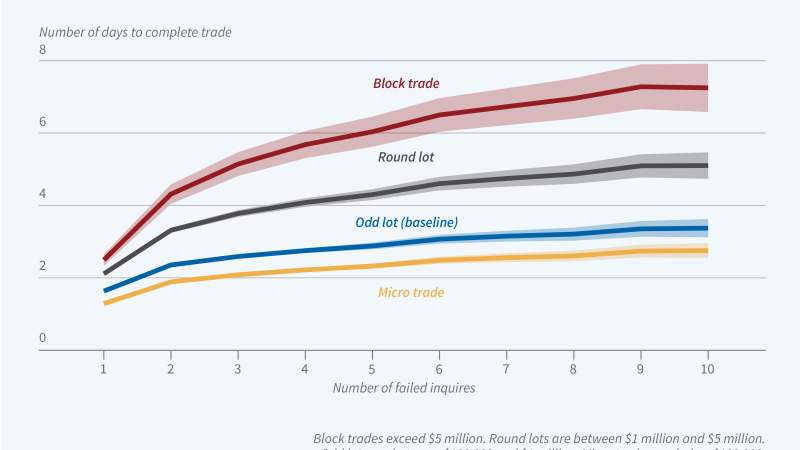

In contrast to stocks that are traded on established exchanges such as the New York Stock Exchange, corporate bonds are traded in over-the-counter (OTC)...

Anecdotal evidence suggests that large datasets collected and analyzed by firms are increasingly important sources of...